������������ Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

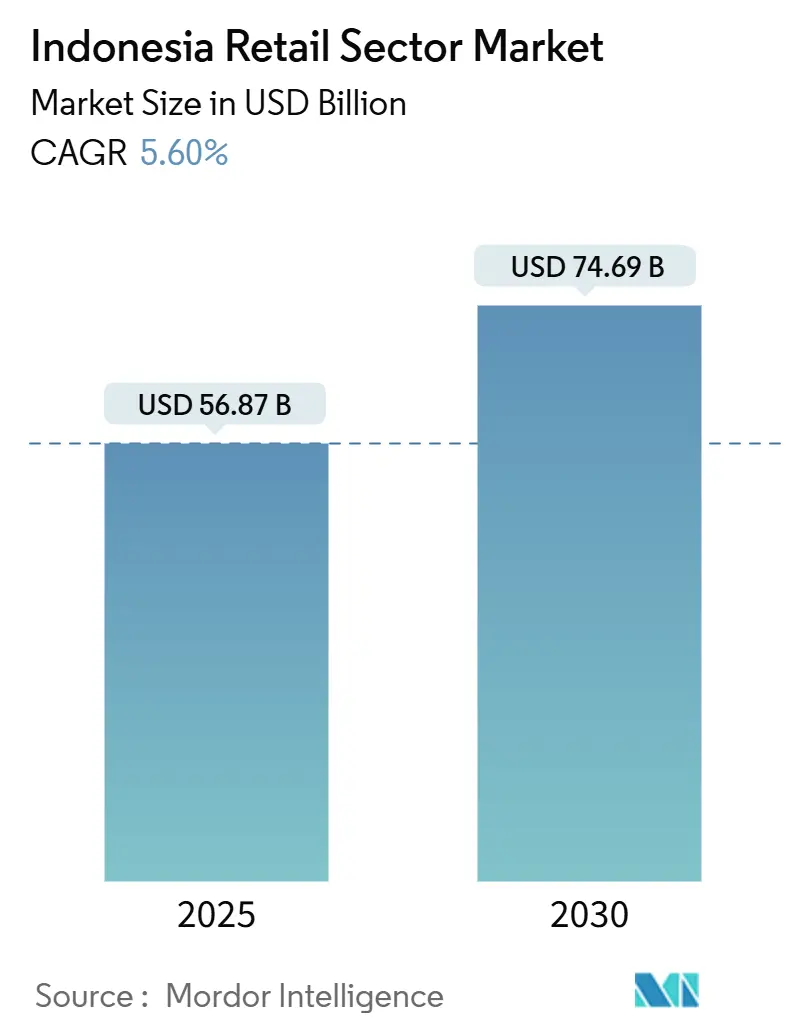

| ������������ Size (2025) | USD 56.87 Billion |

| ������������ Size (2030) | USD 74.69 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

| ������������ Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Retail Sector ������������ Analysis by Mordor Intelligence

The Indonesia retail ������������ generated USD 56.88 billion in 2025 and is projected to reach USD 74.69 billion by 2030, reflecting a 5.6% CAGR. Household spending remains the backbone of growth, accounting for 54% of GDP in 2024, while infrastructure roll-outs under the National Medium-Term Development Plan lower cost-to-serve in secondary cities [1]Source: Badan Pusat Statistik, “Household Consumption Statistics 2024,�� bps.go.id. Digital acceptance keeps expanding as Bank Indonesia’s QRIS standard cuts payment friction, and rising smartphone ownership unlocks mobile commerce for millions of first-time shoppers [2]Source: Bank Indonesia, “QRIS Implementation Report 2024,�� bi.go.id. Modern formats attract capital thanks to liberalized foreign-investment caps, yet the archipelago’s fragmented logistics and deep-rooted “warung�� culture temper the speed of change. Forward-looking operators pivot toward omnichannel models, invest in data-driven merchandising, and localize assortments for price-sensitive consumers beyond Java.

Key Report Takeaways

- By product category, Food and Beverage led with 35.16% of the Retail in Indonesia ������������ size in 2024; Health, Beauty and Personal Care is forecast to expand at a 12.8% CAGR to 2030.

- By distribution channel, Convenience Stores and Mini-������������s held 45.54% of Retail in Indonesia ������������ share in 2024, while Hyper������������s and Super������������s post the highest 9.4% CAGR through 2030.

- By payment method, Cash accounted for 42.50% of transactions in 2024; E-Wallets are advancing the quickest at a 19.2% CAGR.

- By region, Greater Jakarta captured 39.95% of the Retail in Indonesia ������������ in 2024, whereas Sulawesi exhibits the fastest 10.5% CAGR between 2025-2030.

- By top 5 companies such as Indomaret, Alfamart, Shopee Indonesia, Tokopedia, Hypermart / Foodmart holds significant ������������ share in 2024.

Indonesia Retail Sector ������������ Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urban-Middle Class Expansion in Tier-2 Indonesian Cities | 1.8% | National, with strongest impact in Java and Sumatra | Medium term (2-4 years) |

| Government Push for Cashless Society Accelerating Modern Retail Adoption | 1.2% | National, with early gains in Greater Jakarta and major urban centers | Medium term (2-4 years) |

| Rising Penetration of Affordable Smartphones Driving Mobile-First E-commerce | 1.5% | National, with higher impact in urban areas | Short term (�� 2 years) |

| Domestic FMCG Manufacturers' Shift to Direct-to-Retailer Distribution | 0.7% | National, with concentration in Java | Medium term (2-4 years) |

| Relaxation of Foreign Investment Caps in Retail Sub-sectors | 0.9% | National, with focus on major urban centers | Long term (�� 4 years) |

| Tourism Rebound Boosting Bali and Secondary Leisure Retail Hubs | 0.6% | Bali, Nusa Tenggara, and tourist destinations | Short term (�� 2 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This ������������

Download PDF

Rapid Urban-Middle Class Expansion in Tier-2 Indonesian Cities

The urban middle class is surging outside Jakarta. Bappenas estimates 135 million middle-income Indonesians by 2030, reshaping demand in cities such as Surabaya, Semarang, Medan, and Makassar[3]Source: Bappenas, “Middle-Class Projection Study,�� bappenas.go.id. Toll-road extensions and new airports shorten supply lines, allowing modern grocers to promise same-day replenishment. Indonesia retail ������������ players open smaller mall-anchored stores that tailor assortments to regional tastes, often blending national brands with local snack favorites. Consumer finance firms report double-digit growth in installment sales for household appliances, suggesting a shift toward lifestyle purchases beyond essentials.

Government Push for Cashless Society Accelerating Modern Retail Adoption

Bank Indonesia mandates universal QR acceptance, and 15 million micro-merchants joined QRIS in 2024. In modern chains, cash now accounts for 42.50% of transactions, down from 50% two years earlier. E-wallet providers layer loyalty points and micro-savings into apps, encouraging daily use. Retailers favor cashless transactions for faster checkouts and richer shopper data. With a 90% financial-inclusion target by 2025, regulators invest in digital-literacy drives for rural adults, broadening the addressable pool for mobile commerce.

Rising Penetration of Affordable Smartphones Driving Mobile-First E-commerce

Domestic assembly incentives push entry-level 4G handsets below USD 60, making smartphones a mass-������������ staple. Mobile screens host 87.2% of online retail orders and dominate product discovery through live streaming and short video. Indonesia retail ������������ operators optimize lightweight apps that load in limited-bandwidth areas, pairing them with local language chatbots to elevate service quality. Fast-growing categories include beauty, snack foods, and budget electronics, all promoted through influencer-led flash sales that convert viewers within minutes.

Domestic FMCG Manufacturers�� Shift to Direct-to-Retailer Distribution

Local processors of noodles, snacks, and beverages increasingly truck products straight to mini������������ chains, bypassing traditional wholesalers. Lead times drop by 30%, boosting on-shelf freshness and reducing stock-outs. Retailers secure better margins on private-label tie-ups, while producers gather sell-through data that guides flavor innovation. Government trade rules now permit flexible exclusivity agreements provided shelf prices stay competitive.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently High Logistics Costs Across the Archipelago | -1.3% | National, with highest impact in eastern Indonesia | Long term (�� 4 years) |

| Price-Sensitive Consumer Base Limiting Premiumization | -0.8% | National, more pronounced outside major urban centers | Medium term (2-4 years) |

| Fragmented Traditional "Warung" Network Hindering Modern Trade Growth | -1.1% | National, particularly in rural and semi-urban areas | Long term (�� 4 years) |

| Complex Provincial Licensing and Zoning Regulations | -0.7% | National, with varying impact by province | Medium term (2-4 years) |

Source: Mordor Intelligence

Persistently High Logistics Costs Across the Archipelago

Moving goods from Java to Maluku can inflate retail prices by 25%, partly because small-parcel routes rely on return-empty trips. Government sea-toll routes alleviate bulk haulage but not last-mile courier rates. As a result, some online retailers apply location-based surcharges, dampening conversion in remote areas. Large chains explore coastal micro-hubs and drone pilot projects, yet meaningful cost relief hinges on multi-modal infrastructure that remains years away.

Price-Sensitive Consumer Base Limiting Premiumization

A Gini index of 0.382 underscores income disparities. Outside Jakarta, 65% of shoppers cite price as the top purchase driver. Retail in Indonesia ������������ retailers therefore continue “shrink-flation”—selling smaller packs at constant prices—to preserve affordability. Premium lines succeed mainly when bundled with instalment plans or loyalty-based cashback, making aspirational items attainable for lower-middle segments.

Segment Analysis

By Product Category: Health and Beauty Outpaces Staples

Food and Beverage held the largest 35.16% Indonesia retail ������������ share in 2024, anchored by daily staples and rising demand for ready-to-eat meals. Health, Beauty, and Personal Care leads growth with a 12.8% CAGR, supported by halal certification rules that legitimize local cosmetic brands. In-store dermatology counters combine skin analysis with curated regimes, converting single-item shoppers into basket-builders. Traditional snacks like kripik and tempeh chips gain premium placement within mini������������s, reflecting nostalgic appeal even in modern settings.

Over the forecast horizon, gamified wellness programs within e-wallets reward vitamin purchases, nudging shoppers toward preventive health routines. Consumer Electronics and Appliances benefit from smart-home adoption, particularly energy-saving air conditioners promoted under national efficiency standards. Apparel and Footwear experiments with limited-run drops that sync with TikTok trends, and furniture chains pair modular designs with quick-ship promises, reaching younger families furnishing their first homes.

Note: Segment shares of all individual segments are available upon report purchase

By Distribution Channel: Proximity Beats Size, Omnichannel Seamlessly Blends

Convenience Stores and Mini-������������s garnered a 45.54% slice of retail in Indonesia ������������ size in 2024, owing to walkable locations and mix-and-match SKUs that meet daily top-up missions. Hyper������������s and Super������������s, though accounting for a smaller base, deliver a 9.4% CAGR as operators retrofit aisles for gourmet corners and cook-along demos that turn weekly grocery trips into family outings. Pop-up kiosks inside gasoline stations expand convenience reach for commuters.

Digital synergies accelerate: mini������������s host parcel lockers, while hyper������������s run dark-store zones dedicated to two-hour deliveries. Department stores digitize fitting rooms with AR mirrors, rendering them interactive discovery spaces. Traditional warungs integrate POS apps that link to supplier ������������places, widening assortments without incurring heavy inventory risk.

Note: Segment shares of all individual segments available upon report purchase

By Payment Method: Cash Holds Lead but Slips Each Quarter

Cash managed 42.50% of retail payments in 2024. E-Wallets sprint forward with a 19.2% CAGR, converting first-time users through transport and food-delivery ecosystems. QRIS-compliant codes unify acceptance, and peer-to-peer transfers encourage wallet top-ups. Debit and credit cards climb in value terms as shoppers reserve them for higher-ticket goods, aided by zero-interest instalment campaigns.

Retailers adopt dynamic-pricing experiments that offer small e-wallet discounts to soften the inflation bite. Pay-later services bundle with purchase-protection insurance, appealing to risk-averse households. Overall, multi-method acceptance remains critical, but backend integrations expose retailers to rich payment-level data for analytics-driven promotions.

Geography Analysis

Greater Jakarta’s retail stock crossed 4.9 million sq m in 2024, and base rents rose 2.1% despite macro headwinds. Retailers respond with community-centric formats, embedding daycare and wellness clinics alongside stores to boost dwell-time. In Bandung, factory outlet clusters leverage tourism from neighboring provinces, while Yogyakarta’s student population spurs evening-economy sales in grab-and-go coffee chains.

In Sumatra, highway tolling simplifies cross-provincial truck movements, enabling centralized DCs that serve multiple cities within a 12-hour radius. Kalimantan retail sentiment links to the new capital; early adopters include home-improvement giants prepping to supply government housing projects. Sulawesi’s Makassar Port handles rising container volumes, and retailers deepen assortments to meet aspirational shoppers flush with income from nickel-processing jobs.

The tourist belt of Bali and Nusa Tenggara rejoices at a hotel occupancy rebound past 70%. Luxury fashion houses re-open boutiques in Seminyak, while local surf-gear brands piggyback on international foot traffic. Papua and Maluku still lack dense retail networks, yet telecom tower roll-outs enhance online shopping feasibility, allowing e-commerce to leapfrog physical build-outs in the medium term.

Competitive Landscape

Innovation and Digital Integration Drive Growth

For established players to maintain and increase their ������������ share, the focus needs to be on developing integrated retail ecosystems that combine physical retail and digital channels seamlessly. Success factors include investing in advanced analytics capabilities, developing private label products, and creating personalized shopping experiences through loyalty programs and targeted ������������ing. Companies must also strengthen their last-mile delivery infrastructure and implement sustainable practices to meet growing environmental consciousness among consumers, while maintaining cost competitiveness in an increasingly price-sensitive ������������.

New entrants and challenger brands can gain ground by focusing on niche ������������s and specialized product categories that larger players may overlook. The key lies in leveraging digital technologies to reduce operational costs and create differentiated value propositions. Regulatory considerations, particularly regarding foreign investment and e-commerce operations, continue to shape ������������ entry strategies. The risk of substitution remains moderate, primarily mitigated through brand building and customer loyalty programs, while end-user concentration varies significantly across different retail formats and geographical locations, necessitating tailored approaches to ������������ penetration and expansion. The retail trade sector continues to evolve, with brick and mortar retail still playing a crucial role in consumer engagement.

Indonesia Retail Sector Industry Leaders

-

Indomaret

-

Alfamart

-

Shopee Indonesia

-

Tokopedia

-

Hypermart / Foodmart

- *Disclaimer: Major Players sorted in no particular order

Need More Details on ������������ Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: AEON Mall Indonesia launched its fifth site, AEON Mall Deltamas, blending retail, FandB, and community recreation spaces.

- February 2025: Pakuwon Group unveiled Pakuwon Mall Bekasi, expanding Greater Jakarta retail GLA to 3.24 million sq m and underpinning suburban growth.

- December 2024: TikTok Shop resumed Indonesian operations after acquiring a majority stake in Tokopedia, wiring social-commerce features into a leading ������������place.

Indonesia Retail Sector ������������ Report Scope

The report on the Indonesian retail sector provides a comprehensive evaluation of the ������������, with an analysis of the segments in the ������������. Moreover, the report also provides the competitive profile of the key manufacturers, along with regional analysis. The Indonesia retail industry is segmented by products (food and beverages, personal and household care, apparel, footwear, and accessories, furniture, toys, and hobby, electronic and household appliances, and other products) and distribution channel (super������������s/hyper������������s, convenience stores, and department stores, specialty stores, online, and other distribution channels). The report offers ������������ size and forecasts for the retail sector in Indonesia in value (USD million) for all the above segments.

| By Product Category | Food and Beverage |

| Apparel and Footwear | |

| Consumer Electronics and Appliances | |

| Home and Furniture | |

| Health, Beauty and Personal Care | |

| Others | |

| By Distribution Channel | Hyper������������s and Super������������s |

| Department Stores | |

| Convenience Stores and Mini-������������s | |

| Specialty Stores | |

| Traditional (Warung / Kiosks) | |

| Online | |

| By Payment Method | Cash |

| Debit & Credit Cards | |

| E-Wallets | |

| Bank Transfers / Pay-Later | |

| By Region | Greater Jakarta |

| Rest of Java | |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Bali & Nusa Tenggara | |

| Papua & Maluku |

By Product Category

| Food and Beverage |

| Apparel and Footwear |

| Consumer Electronics and Appliances |

| Home and Furniture |

| Health, Beauty and Personal Care |

| Others |

By Distribution Channel

| Hyper������������s and Super������������s |

| Department Stores |

| Convenience Stores and Mini-������������s |

| Specialty Stores |

| Traditional (Warung / Kiosks) |

| Online |

By Payment Method

| Cash |

| Debit & Credit Cards |

| E-Wallets |

| Bank Transfers / Pay-Later |

By Region

| Greater Jakarta |

| Rest of Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali & Nusa Tenggara |

| Papua & Maluku |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Retail in Indonesia ������������ size today?

Indonesia retail ������������ size reached USD 56.88 billion in 2025 and is forecast at USD 74.69 billion by 2030.

Which product category grows the fastest?

Health, Beauty and Personal Care posts a leading 12.8% CAGR from 2025-2030.

How dominant are convenience stores?

Convenience Stores and Mini-������������s held 45.54% of Retail in Indonesia ������������ size in 2024, the largest share among offline formats.

Are cash payments still common?

Yes, cash remains 42.50% of payments, though E-Wallets show the fastest 19.2% CAGR through 2030.

Why is Sulawesi significant for expansion?

Sulawesi records the fastest regional CAGR at 10.5%, driven by port upgrades and mining-led income growth.