Endoscopic Vessel Harvesting ������������ Size and Share

������������ Overview

| Study Period | 2019 - 2030 |

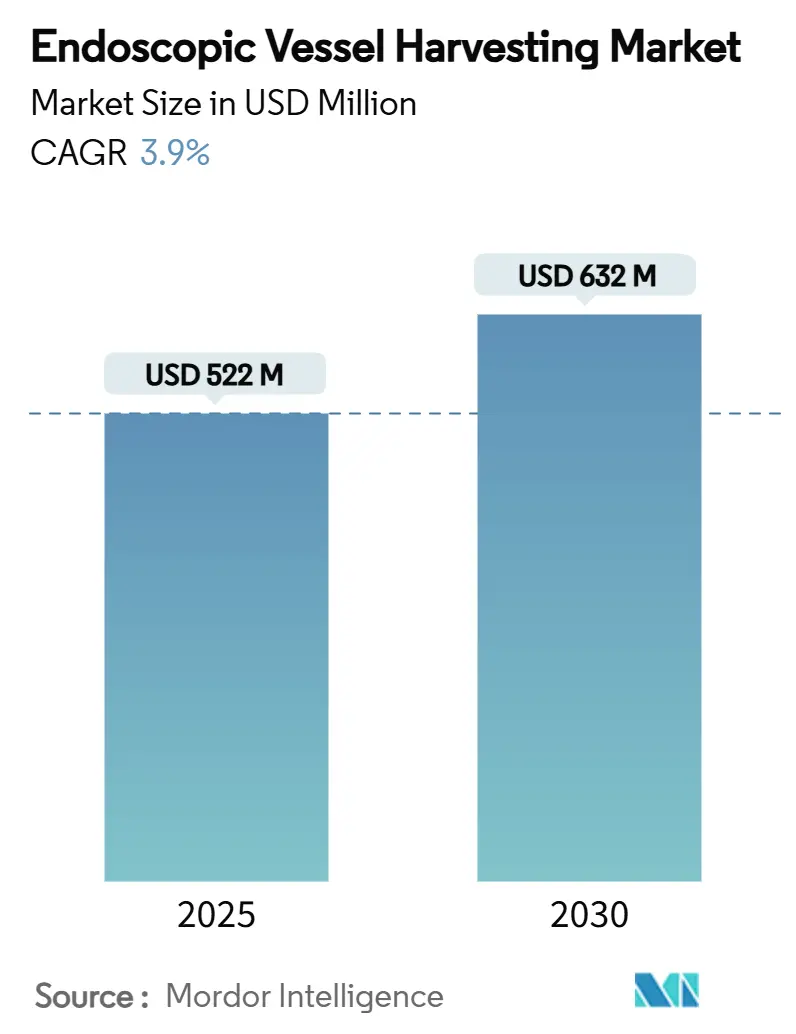

| ������������ Size (2025) | USD 522 Million |

| ������������ Size (2030) | USD 632 Million |

| Growth Rate (2025 - 2030) | 3.90% CAGR |

| Fastest Growing ������������ | Asia Pacific |

| Largest ������������ | North America |

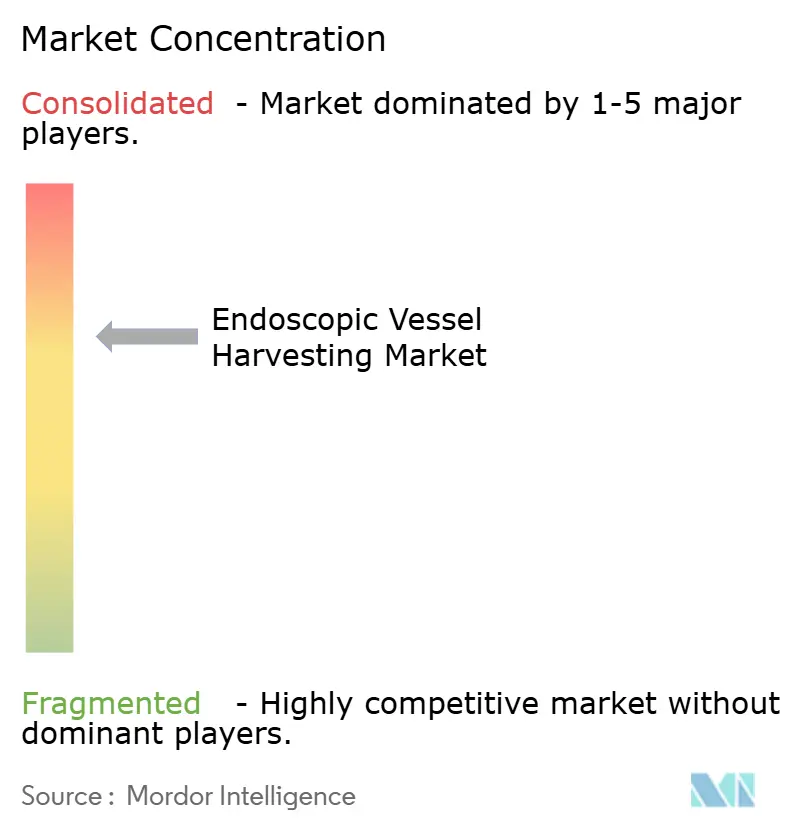

| ������������ Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Endoscopic Vessel Harvesting ������������ Analysis by Mordor Intelligence

The endoscopic vessel harvesting ������������ size reached USD 522 million in 2025 and is projected to attain USD 632 million by 2030, reflecting a 3.9% CAGR. Growing cardiac surgery volumes, heightened surgeon preference for minimally invasive conduit procurement, and steady product innovation all sustain this measured expansion. Demand remains most intense in high-income regions where value-based care frameworks reward shorter stays and lower complication rates. Hybrid platforms that bundle visualization, insufflation, and disposable kits are gaining traction because they simplify procurement and standardize procedural quality. Meanwhile, recent device recalls are prompting hospitals to scrutinize supplier quality systems more closely, encouraging a flight to vendors with strong post-������������ surveillance records.

Key Report Takeaways

- By product type, EVH systems held a 66.35% revenue share in 2024, while accessories and disposables are forecast to grow at an 8.25% CAGR through 2030.

- By vessel type, radial artery harvesting led with 42.53% of the endoscopic vessel harvesting ������������ share in 2024; saphenous vein procedures are expected to expand at a 7.85% CAGR to 2030.

- By usability, disposable devices accounted for 64.62% of the endoscopic vessel harvesting ������������ size in 2024, whereas reusable systems are projected to advance at an 8.52% CAGR between 2025-2030.

- By application, coronary artery disease procedures represented 84.21% of total cases in 2024, while peripheral artery disease interventions are poised for a 7.61% CAGR.

- By end-user, hospitals commanded 58.82% of 2024 revenue, though ambulatory surgical centers are on track to post the fastest growth at 9.82% CAGR.

- By geography, North America contributed 42.82% of 2024 turnover; Asia-Pacific is set to be the fastest-growing territory at 10.13% CAGR.

Global Endoscopic Vessel Harvesting ������������ Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global cardiovascular disease burden | +1.2% | Worldwide, highest in North America and Europe | Long term (�� 4 years) |

| Preference for minimally invasive harvesting | +0.8% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Higher adoption of off-pump CABG surgeries | +0.6% | Global, led by developed ������������s | Medium term (2-4 years) |

| Hospitals�� cost-saving pivot from open EVH | +0.5% | North America and Europe, emerging in Asia-Pacific | Short term (�� 2 years) |

| Simulator-based surgeon training uptake | +0.3% | North America and Europe, selective Asian centers | Medium term (2-4 years) |

| Supply-chain shift from open disposables | +0.2% | Global, concentrated in high-volume hospitals | Short term (�� 2 years) |

Source: Mordor Intelligence

Increasing Global Burden of Cardiovascular Diseases

Cardiovascular pathology affects nearly half of U.S. adults and continues to climb in many emerging economies. Growing procedure volumes make efficient conduit harvesting a strategic necessity for surgical programs managing tight bed capacity and readmission penalties. Hospitals adopting endoscopic techniques report fewer wound infections and faster ambulation, outcomes that align with modern bundled-payment incentives. The burden remains particularly high among aging cohorts with diabetes and hypertension, reinforcing the need for durable grafts and low-morbidity access sites. Governments are channeling funds into cardiac centers of excellence, catalyzing procurement of integrated EVH platforms that promise predictable learning curves and reduced staff turnover. Vendors able to document long-term graft patency and cost offsets stand to benefit most from these epidemiological tailwinds.

Growing Preference for Minimally-Invasive Harvesting

Prospective data show leg wound complications of 0.82% with endoscopic approaches versus 3% for open extraction[1]Maria Cannoletta et al., “Endoscopic Conduit Harvest,�� Journal of Cardiothoracic Surgery, cardiothoracicsurgery.biomedcentral.com. Patient-reported outcome measures consistently favor minimal scarring and quicker mobility, metrics now embedded in many pay-for-performance dashboards. Hospitals ������������ing “scar-sparing�� programs gain reputational lift that translates into higher referral volumes, especially in competitive urban catchments. Widespread adoption of virtual-reality simulation has shortened operator learning curves and cut fluoroscopy exposure times by nearly one-third. Nonetheless, centers must invest in structured mentorship to avoid early complication clusters that can erode surgeon confidence. Device designers are responding with ergonomic handles and automated cutting controls to further flatten proficiency curves.

Rising Adoption of Off-Pump CABG Surgeries

Beating-heart grafting eliminates cardiopulmonary bypass-related inflammatory cascades and has shown lower mortality in patients with moderate renal dysfunction. Off-pump workflows pair naturally with endoscopic conduit harvesting because both seek to minimize physiologic insult. Robotic platforms now facilitate totally endoscopic, anaortic techniques that achieved 97.3% freedom from mitral regurgitation recurrence in a recent Japanese series[2]Tatsuya Tarui et al., “Totally Endoscopic Robotic Repair,�� Circulation Journal, jstage.jst.go.jp. As hybrid rooms proliferate, hospitals bundle off-pump and EVH capabilities into turnkey service lines ������������ed toward high-risk patients. Vendors offering interoperable robotic arms, angioscopes, and insufflation units gain a competitive edge by simplifying capital-budget decisions.

Hospitals�� Cost-Saving Shift from Open to EVH

Secondary analysis of the REGROUP trial placed discharge costs at USD 76,607 for endoscopic versus USD 75,368 for open harvest, suggesting cost neutrality at worst while generating fewer wound-related readmissions. CFOs increasingly view EVH devices as enablers of higher throughput rather than discretionary “nice-to-have�� tools. Volume-based discounts on single-use kits and shared-risk contracts that rebate disposables if complication benchmarks are met are gaining favor. Meanwhile, supply-chain teams value the smaller storage footprint of sealed EVH kits compared with bulky open-harvest drapes and instruments. These operational considerations elevate purchasing criteria beyond unit price toward total-cost-of-ownership models.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative revascularization therapies | -0.9% | Global, highest in advanced ������������s | Medium term (2-4 years) |

| Unfavorable reimbursement in some countries | -0.7% | Europe and emerging economies | Long term (�� 4 years) |

| Class-I recalls denting surgeon confidence | -0.4% | Worldwide, concentrated in North America | Short term (�� 2 years) |

| Steep learning curve & harvester shortage | -0.3% | Global, acute in lower-income regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Availability of Alternative Revascularization Therapies

Rapid improvements in complex percutaneous coronary intervention techniques are siphoning off some multi-vessel cases that once defaulted to coronary artery bypass grafting. Although CABG retains superiority in diabetics and diffuse disease, declining open-heart volumes in certain geographies could curb EVH unit sales. Yet, the remaining surgical cases now skew toward higher-risk profiles where minimally invasive conduit harvest offers outsized benefits. Device makers therefore position EVH as a precision tool for the subset of patients who still require grafts, emphasizing patency and wound-healing advantages versus open techniques.

Unfavorable Reimbursement in Several Countries

Health technology assessment bodies in Europe often demand long-term cost-utility data before issuing broad coverage for new disposables, delaying adoption cycles. While the July 2024 U.S. outpatient prospective payment update added new pass-through codes for select endoscopic technologies, many private insurers still require prior authorization[3]Centers for Medicare & Medicaid Services, “Hospital Outpatient PPS July 2024 Update,�� cms.gov. In emerging ������������s, capital budgets concentrate on cath labs and basic ICU beds, leaving little room for premium harvesting systems. Vendors are countering by launching low-cost towers and rental models that spread acquisition costs over procedure volume.

Segment Analysis

By Product Type: Systems Drive Revenue, Accessories Accelerate Growth

EVH systems generated USD 346 million in 2024, equal to 66.35% of the endoscopic vessel harvesting ������������. Hospitals purchase these capital assets once every 5-7 years, locking equipment vendors into multiyear service contracts. The accessories and disposables category, though smaller in absolute value, is growing at an 8.25% CAGR thanks to its annuity-style revenue that aligns with procedure counts. Bundled kits containing blades, scopes, and CO�� lines simplify case setup and ensure compatibility, a convenience that purchasing managers value.

Recurring consumables are particularly attractive to ambulatory surgical centers that lack onsite sterilization capacity. Meanwhile, competitive differentiation among capital systems now hinges on image resolution, ergonomic handpieces, and analytics dashboards that log usage statistics for credentialing purposes. Getinge’s Hemopro 3 rollout exemplifies this pivot toward safety-enhanced systems designed to reassure surgeons following prior recalls.

Note: Segment shares of all individual segments available upon report purchase

By Vessel Type: Radial Dominance Meets Saphenous Acceleration

Radial artery conduits captured 42.53% of 2024 volume owing to superior 10-year patency, especially in younger and diabetic patients. Surgeons increasingly adopt bilateral radial strategies, boosting system utilization. Conversely, saphenous vein grafting remains indispensable when three or more distal targets must be bypassed, explaining its projected 7.85% CAGR. Evidence supporting no-touch, perivascular-preserving harvest has mitigated early skepticism regarding vein quality.

Device vendors are developing slimmer scopes and lower-pressure insufflation protocols to reduce endothelial trauma, thereby appealing to skeptics who still prefer open harvest for long conduits. Hospitals now run parallel workflows: radial for high-patency needs and optimized saphenous for multi-graft cases, a trend that increases demand for versatile system platforms.

By Usability: Disposables Lead, Reusables Resurge

Single-use kits held 64.62% of 2024 billings, reflecting infection-control priorities. However, the reusable subsegment is rebounding at 8.52% CAGR as sustainability mandates and capital-constrained public hospitals seek lifecycle savings. Manufacturers are extending reprocessing cycles through durable coatings and modular components, lowering per-case depreciation.

Environmental impact assessments, particularly in Europe, now influence tender decisions, requiring vendors to quantify waste reduction. Reusable advocates also highlight smoother instrument articulation compared with some disposable equivalents, a factor surgeons cite when performing delicate radial harvests.

By Application: CAD Dominance Amid PAD Emergence

Coronary artery disease applications accounted for 84.21% of procedures in 2024, mirroring the dominance of CABG in surgical revascularization. PAD-related harvest is smaller but expanding at 7.61% CAGR as peripheral bypasses gain favor for complex limb ischemia. Surgeons treating PAD appreciate the smaller incisions of EVH, which help fragile skin heal faster.

Reimbursement for PAD bypass varies widely, but centers adopting EVH report shorter ward stays that free capacity for lucrative structural-heart cases. Consequently, administrators view EVH as a platform technology transcending coronary indications and supporting broader vascular programs.

By End-User: Hospitals Anchor, ASCs Accelerate

General hospitals still house 58.82% of annual revenue thanks to full-service cardiac units and residency programs that ingest large patient volumes. Yet, ambulatory surgical centers will post the fastest 9.82% CAGR through 2030 as payers steer low-risk CABG candidates to lower-cost settings. EVH enables same-day ambulation and discharge pathways, making it a prerequisite for ASC accreditation in many U.S. states.

Capital-light disposable kits resonate with ASC managers who avoid large sterilizers. At the same time, hospital systems acquiring ASC chains often mandate cross-facility standardization, guaranteeing steady disposable pull-through for selected vendors.

Note: Segment shares of all individual segments available upon report purchase

By Harvesting Technique: CO�� Insufflation Leads, No-Touch Gains

Closed-tunnel CO�� insufflation methods supplied 53.56% of 2024 procedures, underpinned by two decades of clinical familiarity. The newer no-touch approach, which eschews pressurized gas to keep perivascular tissue intact, is rising at a 10.31% CAGR. Early adopters report higher long-term patency in saphenous grafts, convincing multidisciplinary boards to update protocols.

Transitioning to no-touch requires needle-free insufflators and larger working channels, prompting many sites to upgrade towers. Vendors offering conversion kits enjoy first-mover advantage, while training organizations bundle simulation modules to speed uptake.

Geography Analysis

North America generated 42.82% of 2024 turnover, underpinned by robust reimbursement and high procedural density across academic centers and community hospitals. CMS coverage consistently endorses EVH when clinically justified, and bundled-payment pilots reward shorter length of stay. Ongoing FDA engagement, including 510(k) clearances for upgraded systems, keeps innovation pipelines active. Training consortia such as STS and AATS integrate EVH modules into resident curricula, reinforcing widespread competence.

Europe follows with steady uptake driven by data-driven protocols and cross-border trials. Yet, budget caps in single-payer systems delay refresh cycles, compelling vendors to emphasize cost-utility. Scandinavian hospitals pioneered reusable scopes to satisfy environmental directives, a model now emulated in Germany and France. Mediterranean health systems, facing constrained capital budgets, gravitate toward service-leasing contracts that convert upfront equipment outlays into per-procedure fees.

Asia-Pacific is the fastest-growing territory at 10.13% CAGR through 2030, fueled by Japan’s aging population, China’s expanding middle class, and government investments in tertiary cardiac centers. Japanese surgeons have embraced totally endoscopic robotic harvests, setting performance benchmarks admired across the region. Chinese regulators increasingly fast-track cardiac devices deemed essential to public-health goals, but provincial reimbursement remains uneven. India and Southeast Asia show latent demand limited by training bottlenecks; therefore, vendors partner with medical colleges to build harvesting fellowships.

South America records moderate growth, spearheaded by Brazil’s public-private hospital network that undertakes high-volume CABG. Import taxes and currency volatility challenge foreign entrants, encouraging localized production partnerships. The Middle East and Africa present niche opportunities tied to flagship cardiac institutes in the Gulf and South Africa, yet widespread adoption is hampered by limited insurance coverage and surgeon shortages.

Competitive Landscape

������������ concentration is moderate, with the top five manufacturers controlling significant global revenue. Getinge leads on installed base, but its 2024 Class I recall heightened scrutiny of silicone particulate risks, prompting some health systems to dual-source disposables. Terumo capitalized by expanding Puerto Rico manufacturing capacity in 2025, ensuring supply resilience and shortened shipping lanes to U.S. customers.

Strategic acquisitions continue to reshape the landscape. Teleflex’s pending USD 791 million purchase of BIOTRONIK’s vascular intervention unit signals converging interests between coronary, peripheral, and conduit-harvesting portfolios. LivaNova, after positive OSPREY trial results on cardiac tissue viability, is scouting partnerships to integrate perfusion data with real-time endoscopic imaging feeds.

Innovation pipelines emphasize modular devices with AI-assisted dissection tracking and cloud dashboards that log harvest duration, thermal exposure, and graft orientation. Start-ups financed by EU green-tech funds are prototyping biodegradable disposable components to cut medical waste. Larger incumbents respond by offering trade-in credits for hospitals adopting eco-certified kits, a tactic aimed at retaining accounts mindful of CSR targets. Overall, the competitive field balances incremental safety upgrades with ambitious digital-workflow visions.

Endoscopic Vessel Harvesting Industry Leaders

-

Getinge AB

-

Terumo Corporation

-

LivaNova PLC

-

Medical Instruments Spa

-

KARL STORZ SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Cabrini Health became the first private hospital in Victoria to perform endoscopic vein harvesting for coronary bypass patients.

- March 2024: Getinge received FDA 510(k) clearance for Vasoview Hemopro 3, its next-generation endoscopic vessel harvesting system.

Global Endoscopic Vessel Harvesting ������������ Report Scope

As per the scope of the report, endoscopic vessel harvesting devices are used to obtain one or more healthy vessels from the patient's leg or arm to be used as conduits to bypass obstructed blood vessels in the cardiac or peripheral region.

The endoscopic vessel harvesting ������������ is segmented by product, usability, application, and geography. By product, the ������������ is sub-segmented into EVH systems, endoscopes, and accessories. By usability, the ������������ is sub-segmented into disposable and reusable. By application, the ������������ is sub-segmented into coronary artery disease (CAD) and peripheral artery disease (PAD). By geography, the ������������ is sub-segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated ������������ sizes and trends for 17 countries across major global regions. The report offers the value (in USD) for all the above segments.

| By Product Type | EVH Systems | ||

| Endoscopes | |||

| Accessories & Disposables | |||

| By Vessel Type | Saphenous Vein | ||

| Radial Artery | |||

| Others | |||

| By Usability | Disposable | ||

| Re-usable | |||

| By Application | Coronary Artery Disease (CAD) | ||

| Peripheral Artery Disease (PAD) | |||

| By End-user | Hospitals | ||

| Ambulatory Surgical Centers | |||

| Cardiac Specialty Clinics | |||

| By Harvesting Technique | Closed-tunnel CO? insufflation | ||

| No-touch / CO?-free | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| EVH Systems |

| Endoscopes |

| Accessories & Disposables |

| Saphenous Vein |

| Radial Artery |

| Others |

| Disposable |

| Re-usable |

| Coronary Artery Disease (CAD) |

| Peripheral Artery Disease (PAD) |

| Hospitals |

| Ambulatory Surgical Centers |

| Cardiac Specialty Clinics |

| Closed-tunnel CO? insufflation |

| No-touch / CO?-free |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the endoscopic vessel harvesting ������������?

The endoscopic vessel harvesting ������������ size stood at USD 522 million in 2025.

How fast is the ������������ expected to grow?

It is projected to register a 3.9% CAGR, reaching USD 632 million by 2030.

Which region generates the highest revenue?

North America led with 42.82% of global revenue in 2024.

Which product segment is expanding the fastest?

Accessories and disposables are forecast to grow at an 8.25% CAGR through 2030.

Why are ambulatory surgical centers important for future growth?

ASCs adopt endoscopic harvesting to enable same-day CABG discharge, driving a 9.82% CAGR in this end-user segment.