Smart Utilities Management ������������ Size and Share

������������ Overview

| Study Period | 2019 - 2030 |

| ������������ Size (2025) | USD 17.65 Billion |

| ������������ Size (2030) | USD 36.60 Billion |

| Growth Rate (2025 - 2030) | 15.70% CAGR |

| Fastest Growing ������������ | Asia Pacific |

| Largest ������������ | North America |

| ������������ Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smart Utilities Management ������������ Analysis by Mordor Intelligence

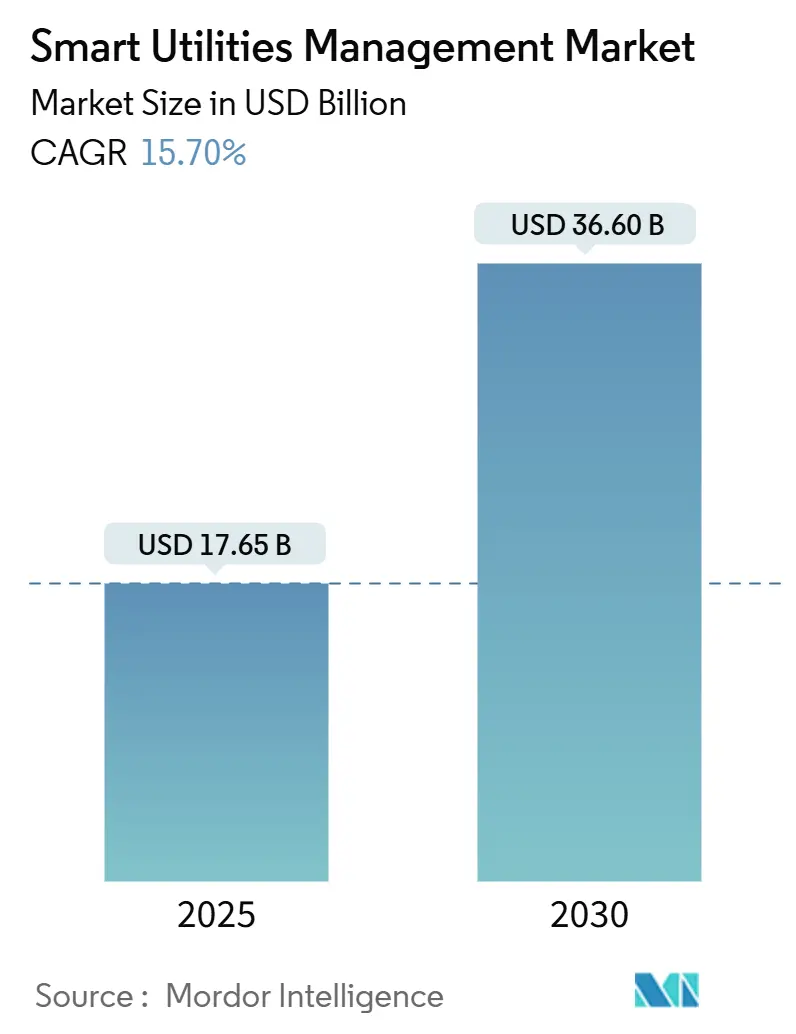

The smart utilities management ������������ size stood at USD 17.65 billion in 2025 and is forecast to reach USD 36.60 billion by 2030 at a 15.7% CAGR, underscoring a clear shift from legacy assets to data-centric, automated grids. Accelerated rollouts of advanced metering infrastructure (AMI), large-scale digital-twin deployments, and edge-enabled analytics are the chief forces sustaining this trajectory. North America remains the largest regional hub on the back of supportive regulation and grid-modernization budgets, while Asia-Pacific registers the fastest expansion as China and India direct record utility capex toward next-generation transmission and distribution. Utilities are also adopting microgrids and distributed energy resource (DER) orchestration platforms to harden networks against climate-driven outages and optimize behind-the-meter assets. Software solutions dominate procurement plans, yet managed services are rising fastest as utilities outsource complex system integration and cybersecurity oversight.

Key Report Takeaways

- By component, software captured 57.5% revenue in 2024, whereas services are poised to advance at a 16.3% CAGR through 2030.

- By type, meter data management systems held 48.3% of smart utilities management ������������ share in 2024; advanced outage management systems are projected to expand at 15.9% CAGR to 2030.

- By utility, the electricity segment accounted for 58.1% share of the smart utilities management ������������ size in 2024, while water utilities are forecast to grow 16.8% annually to 2030.

- By deployment, on-premise platforms represented 67.5% of spending in 2024; cloud rollouts are set to register a 17.2% CAGR over the same horizon.

- By geography, North America led with a 38.6% revenue share in 2024; Asia-Pacific is projected to surge at a 16.0% CAGR through 2030.

Global Smart Utilities Management ������������ Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in smart city deployment | +3.2% | Global, early traction in Singapore, China, India | Medium term (2-4 years) |

| Government mandates for AMI | +4.1% | North America, EU, core APAC | Short term (�� 2 years) |

| Integration of DERs and microgrids | +2.8% | North America, Europe, spill-over APAC | Long term (�� 4 years) |

| Improvements in energy efficiency | +2.3% | Global | Medium term (2-4 years) |

| Expansion of IoT-edge analytics | +1.9% | North America, Europe, emerging APAC | Medium term (2-4 years) |

| Digital-twin adoption for water and gas | +1.4% | North America, Europe, pilot APAC | Long term (�� 4 years) |

Source: Mordor Intelligence

Rise in Smart City Deployment

Smart-city programs are accelerating end-to-end utility digitalization as municipal planners demand integrated power, water, transport, and waste operations. Singapore’s Punggol Digital District is deploying a district-level smart grid that unifies energy, cooling, and mobility data into a single command platform[1]JTC Corporation, “Punggol Digital District to Pilot First District-Level Smart Grid,�� jtc.gov.sg. China’s vehicle-to-grid pilots are using connected electric vehicles to balance local distribution loads, signaling convergence between smart mobility and energy management. In the Middle East, Dubai Electricity and Water Authority committed USD 1.9 billion to its smart-grid roadmap, positioning utilities as digital backbones for city-wide optimization. These initiatives create strong network effects: once foundational telemetry is in place, additional city functions—from traffic lights to waste logistics—can ride on the same data spine, amplifying demand for unified utility platforms.

Government Mandates for Advanced Metering Infrastructure

Legislation is the single most powerful catalyst for near-term rollouts. Australia now requires universal smart meters across the National Electricity ������������ by 2030, declaring them “non-negotiable�� for high-renewable grids. In the United States, the Energy Act of 2020 obliges federal facilities to install advanced water meters capable of daily readings. France’s nationwide Linky program showcases how a mandate can hit 90% household coverage within five years, setting performance benchmarks that ripple into export ������������s. Guaranteed volume commitments give vendors scale to cut unit costs and conform products to common standards, thereby lowering adoption risk for late-moving utilities.

Integration of Distributed Energy Resources (DERs) and Microgrids

DER proliferation is pushing utilities from one-way power delivery to bidirectional orchestration. San Diego Gas and Electric recently energized four islandable microgrids totaling 39 MW of solar generation and 180 MWh of storage to maintain service during wildfire disruptions. EPRI’s open-architecture work with Kraken is distilling new interoperability guidelines so utilities can enroll batteries, EVs, and flexible loads into virtual power plants without vendor lock-in. California Energy Commission studies indicate that small commercial sites pairing rooftop PV with storage can cut annual bills by up to USD 2,500 while enhancing voltage stability. Successful orchestration requires real-time situational awareness, automated dispatch, and settlement engines—capabilities intrinsic to the smart utilities management ������������.

Improvements in Energy Efficiency

Digital demand-side tools are delivering measurable kilowatt-hour savings. New York ISO logged a 16% uplift in registered demand-response capacity for summer 2025 after streamlining enrollment and analytics. California’s WaterWatch platform trimmed electricity use at Moulton Niguel Water District by 4.03%, validating the role of cross-utility data in optimizing pump schedules[2]California Energy Commission, “Building-Scale Solar and Storage Can Cut Bills by USD 2,500,�� energy.ca.gov. Residential heuristic control algorithms are now cutting HVAC energy without sacrificing comfort, removing a historical barrier to consumer uptake. Together, these proof points strengthen the business case for broader rollouts of analytics-rich utility platforms.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost, Security and Integration Challenges for Smart Meters | -2.1% | Global, particularly acute in developing ������������s | Short term (�� 2 years) |

| Complex, Evolving Data-Privacy Regulations | -1.8% | EU, North America, emerging in APAC | Medium term (2-4 years) |

| Interoperability Gaps from Proprietary Ecosystems | -1.5% | Global, with concentration in mature ������������s | Medium term (2-4 years) |

| Rural Dependence on Aging Telecom Infrastructure | -1.2% | Rural areas globally, acute in developing regions | Long term (�� 4 years) |

Source: Mordor Intelligence

High Cost, Security and Integration Challenges for Smart Meters

Total-cost-of-ownership hurdles persist, especially where per-customer revenue is low. Full AMI conversions often require substation upgrades, head-end replacements, and new cybersecurity layers, driving up capex beyond meter hardware. Research published in the National Library of Medicine warns that each connected meter introduces an additional attack vector, expanding the grid’s threat surface. Interoperability suffers when vendors restrict APIs or apply proprietary firmware, as illustrated by Australian debates over closed battery ecosystems that limit participation in grid services. Component shortages, driven by semiconductor supply tightness, are prolonging lead times and inflating prices—factors that utilities in cost-sensitive economies must absorb or pass through to consumers.

Complex, Evolving Data-Privacy Regulations

Utilities straddling multiple jurisdictions face diverging consent, retention, and localization mandates. The U.S. Federal Communications Commission recently clarified that demand-response text alerts do not trigger extra consent hurdles, giving domestic operators breathing space. In contrast, Europe’s GDPR imposes strict opt-in requirements and stiff penalties for violations, obliging utilities to anonymize granular consumption profiles. Emerging Asian frameworks mirror GDPR but add local-storage clauses, compelling multi-cloud strategies that raise architecture complexity. Database re-engineering and continuous compliance audits add recurring opex that can erode return on investment if not budgeted upfront.

Segment Analysis

By Type: Advanced Systems Drive Operational Intelligence

Meter data management systems (MDMS) retained leadership with 48.3% revenue in 2024, underscoring utilities�� priority to collect, validate, and analyze interval readings at scale. The segment’s size also positions it as the anchor for broader analytics modules that feed outage, workforce, and asset-health applications, reinforcing vendor lock-in and fueling platform stickiness. Advanced outage management systems are accelerating at a 15.9% CAGR as utilities confront climate-driven extreme-weather events; AI-enabled topology modeling is shrinking fault-location windows from hours to minutes. CenterPoint Energy’s post-hurricane partnership with Neara highlights how utilities procure cloud-native simulation tools to stress-test networks before storm seasons. As multi-application convergence continues, purchasing decisions increasingly factor a vendor’s ability to harmonize MDMS with SCADA, geographic information systems, and DERMS, driving integrators to bundle modules in unified licenses.

A second-order effect of this convergence is the widening skills gap inside utilities. Operators accustomed to legacy SCADA must now interpret probabilistic forecasts and machine-learning outputs, steering utilities toward training programs or managed-operations contracts. Vendors that position MDMS as the kernel for operational intelligence are capturing downstream revenues in customer engagement, field-service automation, and cyber-response, strengthening the long-term cash-flow profile of the smart utilities management ������������.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Leadership Drives Service Growth

Software accounted for 57.5% of spending in 2024, reflecting the high value assigned to analytics, visualization, and automation layers. Core utility software now embeds no-code dashboards, role-based access, and AI-assisted configuration, reducing commissioning cycles from months to days. Simultaneously, utilities are migrating license models from perpetual to subscription, smoothing opex but enlarging lifetime customer value for vendors. Services, although smaller, are expanding at 16.3% CAGR because integration and cybersecurity demands fall outside traditional utility competencies. Veolia’s collaboration with Mistral AI is emblematic: the firm is embedding generative AI chat interfaces so plant managers can query asset efficiency in natural language, essentially converting domain data into decision support.

Hardware sales remain critical for grid-edge visibility—particularly in emerging ������������s embarking on first-wave smart-meter rollouts—but margins are tightening. Suppliers, therefore, bundle firmware licenses, extended warranties, and managed-upgrade programs to lock in recurring revenue. In parallel, cloud hyperscalers court utilities with sector-specific environments certified for NERC CIP and ISO 27001, lowering perceived risk and accelerating the cloud pivot inside the smart utilities management ������������.

By Utility Type: Electricity Leads While Water Accelerates

Electric utilities controlled 58.1% share of the smart utilities management ������������ size in 2024 as transmission-upgrade cycles, DER-orchestration requirements, and EV-charging build-outs demanded advanced grid software. Regulatory cost-recovery mechanisms in North America and Europe further shorten payback periods, sustaining capital inflows. Water utilities, though traditionally under-digitized, are forecast to grow 16.8% annually as drought pressures and leakage penalties climb. Cairns Regional Council’s roll-out of NB-IoT smart meters illustrates how cloud-native telemetry unlocks daily visibility into consumption anomalies, automating customer alerts and maintenance dispatch.

Gas utilities continue focusing digital budgets on safety: remote pressure monitoring, automatic shut-off valves, and methane-leak detection drones. Although gas remains a smaller revenue pool, cross-vector convergence is rising. Multi-utility conglomerates now negotiate enterprise-wide licenses encompassing power, gas, and water, streamlining analytics across vectors and lowering vendor count. This bundling strategy expands total addressable spending per customer, reinforcing the scale advantages already embedded in the smart utilities management ������������.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Cloud Migration Accelerates

On-premise installations still held 67.5% spending in 2024, reflecting cybersecurity mandates that push critical-infrastructure operators to retain physical control. However, the cloud sub-segment’s 17.2% CAGR signals a decisive migration trend as hyperscalers secure FedRAMP, GDPR, and NERC CIP attestations. Utilities now split workloads: real-time control loops and latency-sensitive protection stay on-site, whereas machine-learning training, historical analytics, and customer portals sit in the cloud. Hybrid architectures also leverage edge gateways to preprocess high-volume sensor feeds, a design that preserves data sovereignty while enabling cloud-based AI refinements.

Cloud economics favor smaller municipal or cooperative utilities that lack the scale to sustain redundant Tier III data centers. Pay-as-you-go compute converts capital expenditure into operating expenses aligned with tariff cycles, easing regulatory approvals. Furthermore, built-in disaster-recovery zones exceed most in-house capabilities, enhancing overall resilience. Collectively, these factors support sustained momentum in cloud adoption, deepening the total lifetime value of the smart utilities management ������������.

Geography Analysis

North America retained 38.6% revenue in 2024 thanks to a synchronized cycle of federal grants, state-level resiliency mandates, and aggressive investor-owned utility (IOU) capex plans. Penetration of AMI exceeds 80% of all meters, shifting attention to DERMS, outage prediction, and customer-centric time-of-use pricing. Europe continues to prioritize decarbonization and energy independence, championing digital twins for capacity planning and cybersecurity hardening across cross-border interties.

Asia-Pacific, however, posts the fastest 16.0% CAGR, anchored by China’s USD 88.7 billion State Grid budget for 2025 and India’s USD 109 billion transmission upgrade blueprint. Governments in the region view digital networks as a prerequisite for large-scale renewable integration and urbanization policies. Vendor strategies, therefore, emphasize cost-optimized hardware, multilingual interfaces, and local-services partnerships to navigate tender rules. Smaller Southeast Asian ������������s replicate early mover playbooks, compressing adoption curves and sustaining above-average growth for the smart utilities management ������������.

Competitive Landscape

The smart utilities management ������������ is moderately consolidated: a cadre of multinational incumbents anchor portfolios spanning meters, head-end software, and advanced analytics, yet specialist disruptors are gaining share in edge AI, cybersecurity, and virtual power plant orchestration. Large players such as Itron, Siemens, and Honeywell scale via technology alliances—NVIDIA for AI inference at the grid edge, EnergyHub for distributed-resource flexibility, or Verizon for 5G connectivity—reducing time-to-������������ for niche capabilities while preserving system-integration revenue.

Investment flows confirm the trend: ABB’s Electrification Ventures stake in Edgecom underscores incumbent appetite for generative-AI startups that complement existing OT-grade software[3]ABB, “ABB Electrification Ventures Invests in Edgecom,�� abb.com. Meanwhile, cloud hyperscalers position industry-specific stacks—complete with digital-twin engines and event-driven data lakes—to win platform deals as utilities enter renewal cycles. Competitive intensity, therefore, revolves less around hardware differentiation and more around ecosystem breadth, partner certification, and cybersecurity credentials.

In emerging ������������s, local system integrators and meter assemblers thrive on price-sensitive tenders, often licensing firmware from global vendors while manufacturing domestically to satisfy localization mandates. This dynamic shifts high-margin software and services revenue toward multinational vendors but keeps hardware volumes local. As utilities pursue multi-vector strategies across electricity, gas, and water, vendors offering truly converged platforms stand to command premium valuations, reinforcing the scale advantages already at play in the smart utilities management ������������.

Smart Utilities Management Industry Leaders

-

IBM Corporation

-

Atos SE

-

Honeywell International Inc.

-

ABB Ltd

-

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Carrier Global and Google Cloud allied to deliver AI-enabled home-energy platforms combining WeatherNext forecasting with battery-supported HVAC optimization.

- March 2025: Itron partnered with NVIDIA to embed edge AI across its Grid Edge Intelligence portfolio, enhancing fault prediction and DER visibility.

- March 2025: WeaveGrid joined with Emporia Energy to widen access to smart EV charging programs across U.S. utilities.

- March 2025: Honeywell integrated Verizon 5G radios into its next-generation meters for real-time remote data acquisition.

Global Smart Utilities Management ������������ Report Scope

Smart utility network is the culmination of three different but mostly interconnected segments, namely smart meter/advanced metering infrastructure (AMI), smart consumer applications, and grid-level applications. It is further divided into meter data management system, energy monitoring/management, smart distribution management.

| By Type | Meter Data Management Systems | |||

| Energy Monitoring / Management | ||||

| Smart Distribution Management | ||||

| Advanced Outage Management Systems | ||||

| By Component | Hardware | |||

| Software | ||||

| Services | ||||

| By Utility Type | Electricity | |||

| Water | ||||

| Gas | ||||

| By Deployment Mode | On-Premise | |||

| Cloud | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Egypt | ||||

| Nigeria | ||||

| Rest of Africa | ||||

| Meter Data Management Systems |

| Energy Monitoring / Management |

| Smart Distribution Management |

| Advanced Outage Management Systems |

| Hardware |

| Software |

| Services |

| Electricity |

| Water |

| Gas |

| On-Premise |

| Cloud |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the smart utilities management ������������?

The ������������ is valued at USD 17.65 billion in 2025 and is projected to rise to USD 36.60 billion by 2030.

Which component segment is growing fastest?

Services lead growth with a 16.3% CAGR because utilities increasingly outsource integration, cybersecurity, and analytics expertise.

Why are water utilities adopting smart platforms more quickly now?

Rising drought pressures, leakage penalties, and NB-IoT metering pilots—such as Cairns Regional Council’s program—are accelerating digital investment in the water segment.

How are government mandates influencing adoption?

National rollouts like Australia’s 2030 smart-meter deadline and the U.S. federal metering requirements create guaranteed demand, enabling scale efficiencies and faster deployments.

What role does edge computing play in utility modernization?

Edge AI embedded in meters or substations minimizes decision latency, cuts backhaul bandwidth by up to 90%, and supports real-time applications such as EV-charging orchestration.

Which region is expected to grow fastest through 2030?

Asia-Pacific is forecast to expand at a 16.0% CAGR, buoyed by China’s record grid investment and India’s large-scale transmission upgrades.