������������ Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

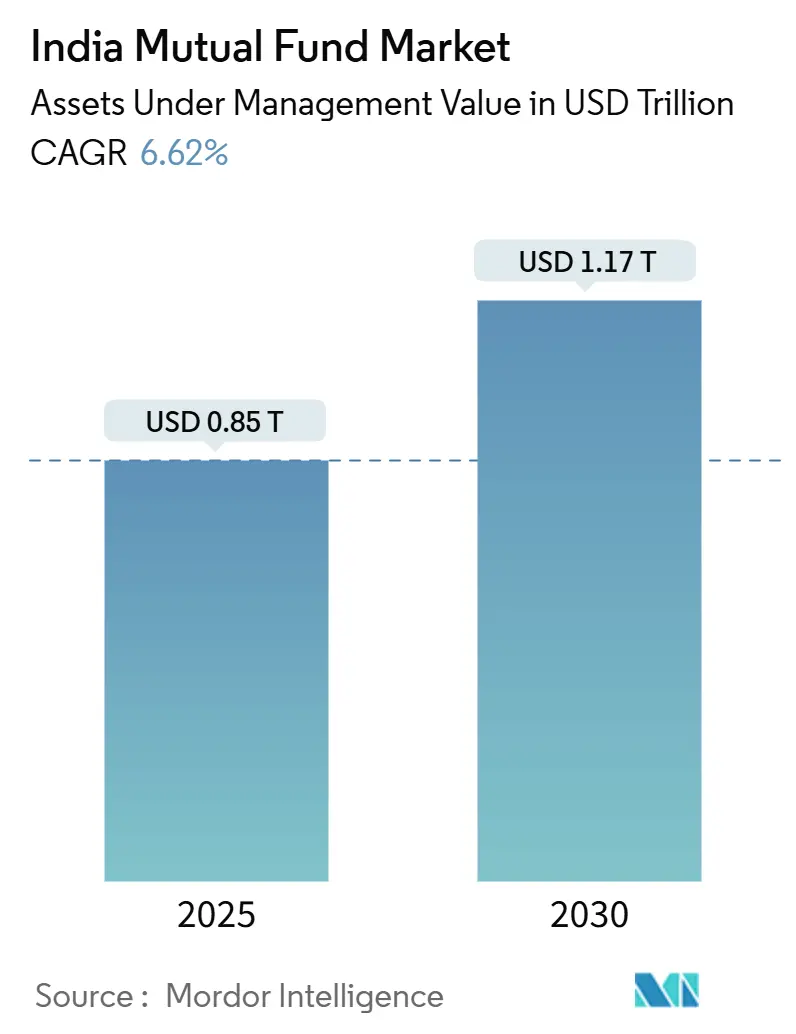

| ������������ Size (2025) | USD 0.85 Trillion |

| ������������ Size (2030) | USD 1.17 Trillion |

| Growth Rate (2025 - 2030) | 6.62% CAGR |

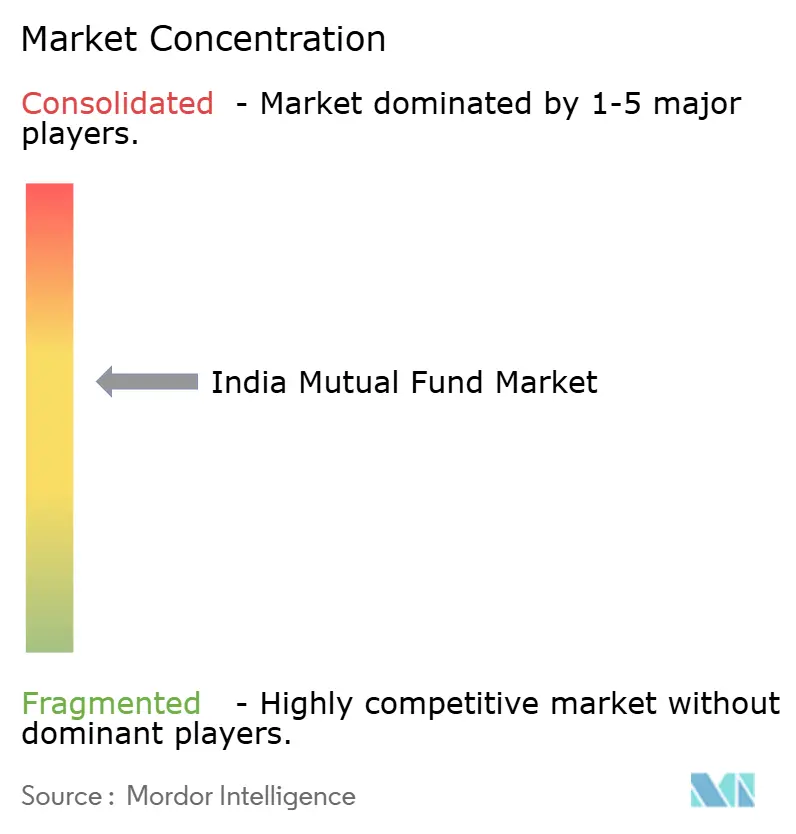

| ������������ Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Mutual Fund ������������ Analysis by Mordor Intelligence

The India mutual fund ������������ is valued at USD 0.85 trillion in 2025 and is projected to touch USD 1.17 trillion by 2030, reflecting a 6.62% CAGR. This healthy momentum stems from a confluence of regulatory modernization, digital distribution, and an enduring retail investment culture that took firmer root after the pandemic. New frameworks such as Specialized Investment Funds (SIFs) and Mutual Fund Lite have expanded the investable universe, bridging classic pooled vehicles with portfolio-management-style products while lowering operating hurdles for passive fund specialists. Equity funds continue to anchor the India mutual fund ������������ as investors increasingly shift household savings away from fixed-income deposits toward long-horizon wealth creation[1]Arijit Ghosh, “Retail SIP Inflows Hit Fresh Record,�� business-standard.com. Rapid penetration of UPI-enabled micro-SIPs, coupled with growing comfort among first-time investors who use mobile apps for onboarding, reinforces steady inflows even in volatile ������������s. Although stricter expense-ratio ceilings and cybersecurity compliance add cost pressure, most asset managers consider technology investments and scale-driven efficiencies adequate countermeasures.

Key Report Takeaways

- By fund type, equity captured 58.97% of the India mutual fund ������������ share in 2024 and is projected to advance at an 8.03% CAGR through 2030.

- By investor type, retail investors held 60.65% share of the India mutual fund ������������ in 2024, while their assets are expected to expand at a 7.24% CAGR to 2030.

- By management style, active funds accounted for 74.19% share of the India mutual fund ������������ in 2024; passive strategies are projected to grow at an 8.56% CAGR.

- By distribution channel, online trading platforms secured a 33.16% share of the India mutual fund ������������ in 2024 and are anticipated to lead growth at 9.15% CAGR.

India Mutual Fund ������������ Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising retail participation via SIPs | +1.8% | National; early gains in B30 cities | Medium term (2-4 years) |

| Rapid digital distribution via fintech & RIA | +1.2% | Urban cores expanding to semi-urban areas | Short term (�� 2 years) |

| Favorable tax incentives for equity funds | +0.9% | National | Long term (�� 4 years) |

| Regulatory push for transparency & lower cost | +0.7% | National | Medium term (2-4 years) |

| Shift of pension assets to long-duration debt | +0.5% | National; organized-sector concentration | Long term (�� 4 years) |

| Micro-SIPs through UPI in Tier-3/4 towns | +0.4% | Rural and semi-urban India | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising Retail Participation via SIPs

Monthly SIP inflows climbed to INR 26,632 crore in April 2025—an all-time high despite equity-������������ swings[2]Press Trust of India, “Equity Fund Inflows Double in FY25,�� rediff.com. SIP-linked AUM has reached 20.31% of industry assets, while active SIP accounts now exceed 8.11 crore, underscoring disciplined investor behavior during corrections. Ticket sizes are also trending higher, lifting average monthly contributions to INR 24,113 crore in FY 2024-25 and paving the way for INR 40,000 crore by 2027. Predictable cash receipts let fund houses extend investment horizons and curb redemption risk, which in turn supports portfolio resilience across ������������ cycles. These structural improvements elevate the long-run growth ceiling for the India mutual fund ������������.

Rapid Digital Distribution via Fintech & RIA Platforms

Digital-first distributors are winning the bulk of new accounts thanks to gamified mobile journeys, vernacular investor-education content, and low-value micro-SIPs that start at INR 100. UPI integration now permits same-day liquid-fund redemptions, effectively positioning select fintech apps as high-yield payments wallets that rival conventional savings accounts[3]Shailaja Sharma, “Fintechs Power Surge in Micro-SIPs,�� livemint.com. The JAM trinity’s ubiquitous identity rails compress onboarding times and acquisition costs, broadening the addressable base to younger, first-time savers. Nonetheless, new rules under the Digital Personal Data Protection Act 2024 impose tougher consent and storage mandates that could delay certain innovations. Even so, the trajectory remains solidly positive for digital adoption across the India mutual fund ������������.

Favorable Tax Incentives for Equity Funds

Revisions to capital-gains slabs in 2024, which nudged short-term rates to 20% and long-term rates to 12.5% while raising the LTCG exemption threshold, enhance the relative post-tax appeal of equity schemes over bank deposits. Equity-Linked Savings Schemes maintain Section 80C relevance and lock in retail capital for three years, delivering stable AUM pools that help managers plan multi-cycle strategies. Because interest from fixed deposits remains taxed annually, the delta after-tax returns further tilt the saver preference toward mutual funds. Younger salaried workers in higher tax brackets feel this benefit most acutely, accelerating flow migration into the India mutual fund ������������.

Regulatory Push for Transparency & Lower Costs

SEBI’s Specialized Investment Fund rules introduced an INR 1 million minimum ticket but kept mutual-fund-like expense caps, granting sophisticated investors broader strategy choice without portfolio-management fees. The Mutual Fund Lite regime similarly lowers entry barriers for passive houses, expanding index-tracking competition that should compress costs further. A forthcoming mandate to disclose every rupee of spend inside the total expense ratio abolishes hidden pass-throughs, sharpening price comparison for consumers. Simultaneously, a uniform Aadhaar-based KYC architecture, mandated for rollout in January 2025, slashes redundancy and makes the India mutual fund ������������ more efficient at scale.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Equity-������������ valuation volatility | ��1.1% | National; sharper in metro investor bases | Short term (�� 2 years) |

| SEBI caps on total-expense ratios | ��0.8% | National | Medium term (2-4 years) |

| Liquidity stress in small-cap funds | ��0.6% | National; scheme-specific concentration | Short term (�� 2 years) |

| Heightened cybersecurity & data-privacy risk | ��0.4% | National; heavier on digital-first distributors | Medium term (2-4 years) |

Source: Mordor Intelligence

Equity-������������ Valuation Volatility Deterring Inflows

Just 300,000 new folios were added in April 2025—the weakest print in 22 months—after indices corrected, illustrating the sensitivity of first-time investors to price swings. Inflows into sector-thematic funds collapsed 97% month-on-month, while redemptions spiked 55%, demonstrating episodic ������������-timing behavior that runs counter to wealth-compounding principles. Fund managers now guide for single-digit equity returns, hinting at a time-based correction that could test investor endurance. With new client acquisition skewed to metros, sentiment cycles in urban hubs can quickly ripple through the India mutual fund ������������. Even so, continuing SIP commitments from existing investors temper the downside and keep cash funnels intact during drawdowns.

SEBI Caps on Total-Expense Ratios Squeeze Margins

Equity scheme TERs now top out at 2.25% on the first INR 500 crore of AUM and taper thereafter, while debt funds sit at 2.00%, reducing the fee headroom that once underwrote high distributor commissions. Because all costs must be embedded in TER, prior ancillary charges have vanished, compelling asset managers to hunt for scale or digital efficiencies. Direct-plan adoption thus rises, cannibalizing regular-plan spreads and forcing cost realignment in advisory channels. Mutual Fund Lite regulations lower hurdles for passives, injecting added competitive pressure on legacy providers and potentially accelerating consolidation within the India mutual fund ������������.

Segment Analysis

By Fund Type: Equity Dominance Accelerates Digital Shift

Equity funds controlled 58.97% of the India mutual fund ������������ size in 2024 and logged an 8.03% CAGR forecast outlook, underscoring the asset class’s central role in the India mutual fund ������������ size expansion toward 2030. Record net inflows in FY 2025 reveal sustained conviction in equities as household allocations steadily move away from legacy term deposits. Bond funds attract conservative capital, buoyed by 6.8%��7% yields that brought a 24% AUM lift in 2024, while hybrid strategies broaden diversification, with multi-asset products now 12% of that category.

Demographic dividends provide additional lift: millennials and Gen-Z investors overwhelmingly favor automated SIPs, supplying long-duration cash that helps managers ride volatility. Specialized Investment Funds, offering long-short and sector-rotation strategies, broaden their SKU range. They do so at a fraction of the minimums set by Portfolio Management Services (PMS), bolstering equity's dominant position in India's mutual fund landscape.

Note: Segment shares of all individual segments available upon report purchase

By Investor Type: Retail Revolution Transforms ������������ Dynamics

Retail investors commanded 60.65% of the India mutual fund ������������ size in 2024 and exhibit a 7.24% CAGR over the forecast period, confirming their primacy in the India mutual fund ������������ share story through 2030. Unique investor counts crossed 54.6 million by April 2025, yet penetration is only 3.6% of the population, suggesting vast headroom for inclusion. Women now make up 26% of folio holders, showing that financial literacy efforts bear fruit across demographics.

Institutional investors still anchor debt and liquid schemes, offering ballast in corrections. However, pervasive micro-SIPs via UPI and tier-3 uptake expand the retail pie faster, gradually diluting institutional dominance. Behavioral stickiness from automated deductions limits knee-jerk redemptions, enabling managers to execute multi-cycle strategies that nurture the India mutual fund ������������.

By Management Style: Passive Strategies Gain Momentum Despite Active Dominance

Active mandates held 74.19% of the India mutual fund ������������ size in 2024, but index funds and ETFs are expected to compound at 8.56% over the forecast period—the highest among style cohorts—signaling growing cost sensitivity and index-tracking comfort. Passive folios doubled in 2024, and ETF assets climbed 37%, aided by 116 new product launches that include thematic baskets such as technology and healthcare. Low-fee structures and SEBI’s Lite framework amplify competition, making passive adoption a structural—not cyclical—theme within the India mutual fund ������������.

Active managers respond by sharpening factor-based stock selection and enhancing disclosure to justify fees, yet systematic underperformance in select categories gives retail investors powerful proof points in favor of passives. Over time, transparent fee differentials and scaling benefits could rebalance the India mutual fund ������������ size mix toward index-tracking vehicles, though active skill remains prized in less efficient segments such as small-caps.

By Distribution Channel: Digital Platforms Disrupt Traditional Models

Online platforms now distribute 33.16% of assets and post a 9.15% CAGR, a trajectory that directly challenges bank-branch dominance in the India mutual fund ������������. Fintechs leverage vernacular content, intuitive UI, and zero-paper onboarding to convert young savers, while robo-advisory nudges encourage timely rebalancing. Banks retain heft in tier-2/3 territories where branch trust still resonates, yet even there, hybrid “phygital�� models are rising.

Brokerage houses cross-sell to equity-trading clients, and independent advisors differentiate through high-touch planning for affluent customers. The JAM rails and UPI micro-transactions cement the distribution democratization, with fintech wallets increasingly embedded as day-to-day finance hubs that route surplus cash into liquid schemes. As scale builds, operating leverage keeps acquisition costs low, positioning digital channels as the growth bedrock of the India mutual fund ������������.

Geography Analysis

Metropolitan centers still hold the lion’s share of AUM, yet the growth spotlight has shifted to smaller towns that contribute to a considerable share of individual assets. SIP penetration maps this trend: while B30 ticket sizes trail their T30 counterparts, B30 account counts are climbing faster, underscoring inclusivity gains. The “Mutual fund sahi hai�� public-awareness campaign continues to resonate across media dark zones, driving curiosity that digital KYC workflows quickly convert into active folios.

Several low-base states have posted triple-digit percentage jumps in average AUM, albeit from modest starting points, hinting at latent upside as economic growth and internet penetration converge. Western and northern corridors remain top contributors relative to state GDP, but the share gap is narrowing as southern and eastern belts ramp up, helped by vernacular fintech outreach and government-led financial-inclusion drives.

Asset managers increasingly seed branch-light kiosks and partnership models in semi-urban clusters, recognizing that future unit economics favor hybrid servicing layered atop mobile self-service. Over half of new SIP accounts now originate outside tier-1, diversifying inflow sources and tapering metro-driven volatility in the India mutual fund ������������.

Competitive Landscape

India’s mutual fund arena shows moderate concentration, with a handful of entrenched houses retaining clear AUM leads even as fresh entrants and digital disruptors intensify rivalry. Strategic moves reshape the leader board: Hinduja Group’s 60% purchase of Invesco India offers an expanded distribution lattice, while the Jio-BlackRock partnership fuses global index prowess with a national telecom reach that could redefine scale economics. Older fund houses confront expense headwinds and passive fee wars, prompting operating-margin resets and process automation to stay competitive.

Technology capabilities now differ widely across managers. Fintech-native challengers win younger demographics through design-first interfaces and real-time analytics, whereas legacy managers accelerate cloud migrations and data-science hires to close that gap. Product innovation is equally intense: ESG, quantitative, and factor strategies proliferate, targeting savvy investors who seek differentiated alpha-sources beyond vanilla diversified funds.

Regulatory tailwinds open additional fronts. SIF guidelines allow managers to combine hedge-fund-style mandates with mutual-fund cost structures, spawning niche skills in long-short or sector-rotation spaces. Passive specialists under Mutual Fund Lite face lower seed-capital thresholds, encouraging boutique index designers to join the India mutual fund ������������ and chip away at incumbents�� share. Overall, competitive gravity favors well-capitalized, tech-savvy firms that can sustain thin fees, high compliance, and customer-experience leadership.

India Mutual Fund Industry Leaders

-

SBI Mutual Fund

-

HDFC Mutual Fund

-

ICICI Prudential Mutual Fund

-

Nippon India Mutual Fund

-

Aditya Birla Sun Life Mutual Fund

- *Disclaimer: Major Players sorted in no particular order

Need More Details on ������������ Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Jio BlackRock Asset Management unveiled its website and leadership team, led by CEO Sid Swaminathan, after obtaining SEBI approval in May 2025.

- June 2025: Motilal Oswal Mutual Fund launched India’s first BSE 1000 Index Fund, opening for subscription 5��19 June 2025.

- May 2025: Edelweiss AMC introduced Altiva SIF, among the first offerings under SEBI’s Specialized Investment Fund rules.

- February 2025: SEBI formally adopted Mutual Fund Lite and SIF regulations through the Third Amendment Regulations 2024.

India Mutual Fund ������������ Report Scope

Mutual funds are pooled investments from many investors to invest in various asset classes. A mutual fund can be a corporation's pension or an employee-owned company's savings plan, or an individual or family can manage it. The report explains the Indian mutual fund industry, regulatory environment, MF companies, and business models. The report also provides a detailed ������������ segmentation with the product types, current ������������ trends, changes in ������������ dynamics, and growth opportunities. Furthermore, an in-depth analysis of the ������������ size and forecasts for the various segments are presented. The Indian Mutual Fund Industry is segmented based on asset class, and source of funds. By asset class, the ������������ is segmented into debt-oriented schemes, equity-oriented schemes, money ������������, ETFs, and foods. By source of funds,the ������������ is segmented into banks, retail investors, Indian institutional investors, FIIs, insurance companies, and other sources. The ������������ size and forecasts are provided in terms of value (USD) for all the above segments.

| By Fund Type | Equity |

| Bond | |

| Hybrid | |

| Money ������������ | |

| Others | |

| By Investor Type | Retail |

| Institutional | |

| By Management Style | Active |

| Passive | |

| By Distribution Channel | Online Trading Platform |

| Banks | |

| Securities Firm | |

| Others |

By Fund Type

| Equity |

| Bond |

| Hybrid |

| Money ������������ |

| Others |

By Investor Type

| Retail |

| Institutional |

By Management Style

| Active |

| Passive |

By Distribution Channel

| Online Trading Platform |

| Banks |

| Securities Firm |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the India mutual fund ������������?

The industry manages USD 0.85 trillion in 2025 assets and is forecast to reach USD 1.17 trillion by 2030.

Which fund category holds the largest India mutual fund ������������ share?

Equity funds lead with a 58.97% share in 2024 and remain the fastest-growing category at an 8.03% CAGR through 2030.

How fast are passive funds growing in the India mutual fund ������������?

Passive strategies such as index funds and ETFs are projected to expand at 8.56% CAGR, the quickest among management styles.

Why are online platforms gaining distribution share?

Fintech interfaces, UPI-enabled micro-SIPs, and low onboarding friction have driven online channels to 33.16% ������������ share and 9.15% CAGR.

What regulatory changes are shaping the ������������ outlook?

SEBI’s Specialized Investment Fund and Mutual Fund Lite frameworks, plus tighter total-expense-ratio rules, are fostering transparency, new products, and cost competition.

How significant are B30 cities for future growth?

Investors beyond the top 30 cities now account for more than 20% of retail assets, highlighting a strong geographic diversification trend that underpins long-term inflows.